When it comes to managing your money, there’s no one-size-fits-all budget. The best system depends on how you earn, spend, and save. Here’s a breakdown of three popular budgeting methods — Zero-Based, Envelope, and 50/30/20 — so you can decide which fits your lifestyle best.

1. Zero-Based Budgeting: Every Pound Has a Job

How it works:

In a zero-based budget, your income minus your expenses equals zero at the end of each month. That doesn’t mean you spend everything — it means you assign every pound to a purpose: spending, saving, debt repayment, or investing.

Example:

If you earn £2,000, you might allocate:

-

£900 for bills

-

£500 for essentials (food, transport)

-

£400 for savings/investments

-

£200 for leisure

Pros:

-

Gives total control over spending.

-

Ensures no money “disappears” unnoticed.

-

Great for people focused on goals like debt payoff or saving milestones.

Cons:

-

Time-consuming to track every category.

-

May feel restrictive for those with irregular incomes.

Best for: detail-oriented planners who like structure and accountability.

2. Envelope Budgeting: Cash in Control

How it works:

This is the classic hands-on method. You divide your income into envelopes (physical or digital) for different spending categories — e.g., groceries, fuel, entertainment. When an envelope is empty, that’s it until next month.

Example:

-

£300 → groceries

-

£100 → transport

-

£50 → entertainment

Pros:

-

Visually limits overspending.

-

Builds strong awareness of habits.

-

Simple and effective for managing day-to-day expenses.

Cons:

-

Harder to use in a cashless world.

-

Not ideal for fixed bills or online purchases.

Best for: those who struggle with impulse spending or want a tactile system.

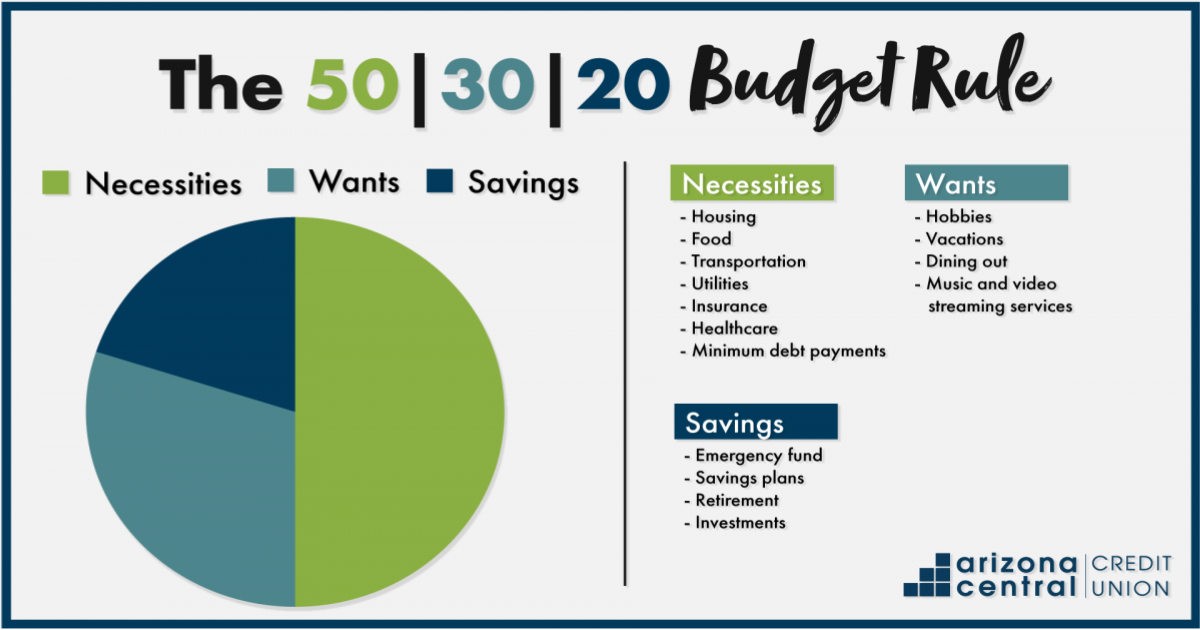

3. 50/30/20 Budgeting: The Balanced Rule

How it works:

This modern approach splits your after-tax income into three broad categories:

-

50% Needs: rent, bills, food, transport

-

30% Wants: entertainment, dining out, subscriptions

-

20% Savings/Debt Repayment: emergency fund, retirement, extra payments

Example (on £2,000 income):

-

£1,000 → Needs

-

£600 → Wants

-

£400 → Savings

Pros:

-

Easy to understand and maintain.

-

Encourages consistent saving habits.

-

Works well for people starting their financial journey.

Cons:

-

Can be too general for complex finances.

-

Ratios may not fit high-cost areas like London or Manchester.

Best for: beginners or those wanting a simple, flexible system.

Which Should You Choose?

-

Pick Zero-Based if you love detailed tracking and goal-oriented budgeting.

-

Try Envelope Budgeting if you overspend easily and need visual limits.

-

Go with 50/30/20 if you want a straightforward, low-effort plan that keeps things balanced.

Final Tip

No matter which method you choose, the real key is consistency. Revisit your budget every month, track your spending, and adjust as your income or priorities change.